Granger causality is a phenomenon where there exists a causal relationship between

two or more different time series data. Complex data sets involving stock market

has higher probability of such problems since the stock price of one company

can be highly dependent on the rise and fall of its competitor.

In this project, we have delved deep to identify non-linear causality between such companies using a deep neural network. There are two main implementations done i) Feed

Forward network with Group Lasso and ii) LSTM network with Group Lasso.

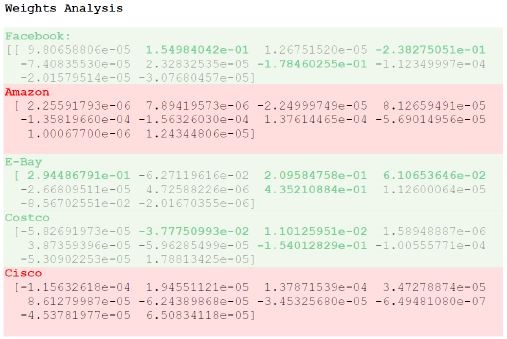

Each of the above architecture is designed in such a way that the weights of

competitor stocked can be interpreted and checked if they are significant in the

final predicted value. We used the stocks of EBay, Amazon, and Apple for predicting the stocks of Facebook. We got non-zero weights values for EBay, Amazon, and Apple thus indicating Granger Causality.

Conclusion

Analyzing two different methods using Multi-Layered Perception (MLP) and

LSTM using group Lasso technique, it seen that each of them have pros and

cons. While MLP is simple and more interpretable, it needs the number of lag

variables pre-specified. The LSTM, although a bit complex learns the number

of lag variables required for the final prediction once it is provided with K - lag

values.

Thus, we would like to conclude saying that building the right model by selecting the best hyper parameters helped in identifying Granger causal relationship even in a constantly varying dataset like stock prices. This implementation

could be used in various other domains having more predictable outcomes to identify such relationship with a very high accuracy.

| Project Report: | See |